What is blockchain? How blockchain technology works

All your burning questions about blockchain technology. How does blockchain work and what problems does it solve? Find out in this easy guide.

By Milly Fox-Jones

Blockchain technology is used to validate and store information digitally on what’s known as a “distributed ledger”. Since it’s based on a peer-to-peer network, blockchain removes the need for a central authority–it’s a decentralized, self-organizing structure.

While most commonly associated with cryptocurrency, blockchain technology has a wide range of applications thanks to its security and efficiency.

This beginner’s guide to blockchain explains what the technology is, how it works, and ways that it can be put to use in areas other than cryptocurrency.

What is blockchain?

Blockchain is a distributed ledger used to validate and record information digitally. A blockchain ledger is essentially a database that's spread and shared across multiple peer-to-peer devices (“nodes”) which are, in turn, spread across multiple people, geographies, time zones, and so on.

All of these computers can access the data and make updates or verifications in real time, visible to everyone – almost like a shared document. Unlike a shared document, though, none of the information can be changed or deleted once it's stored on the blockchain.

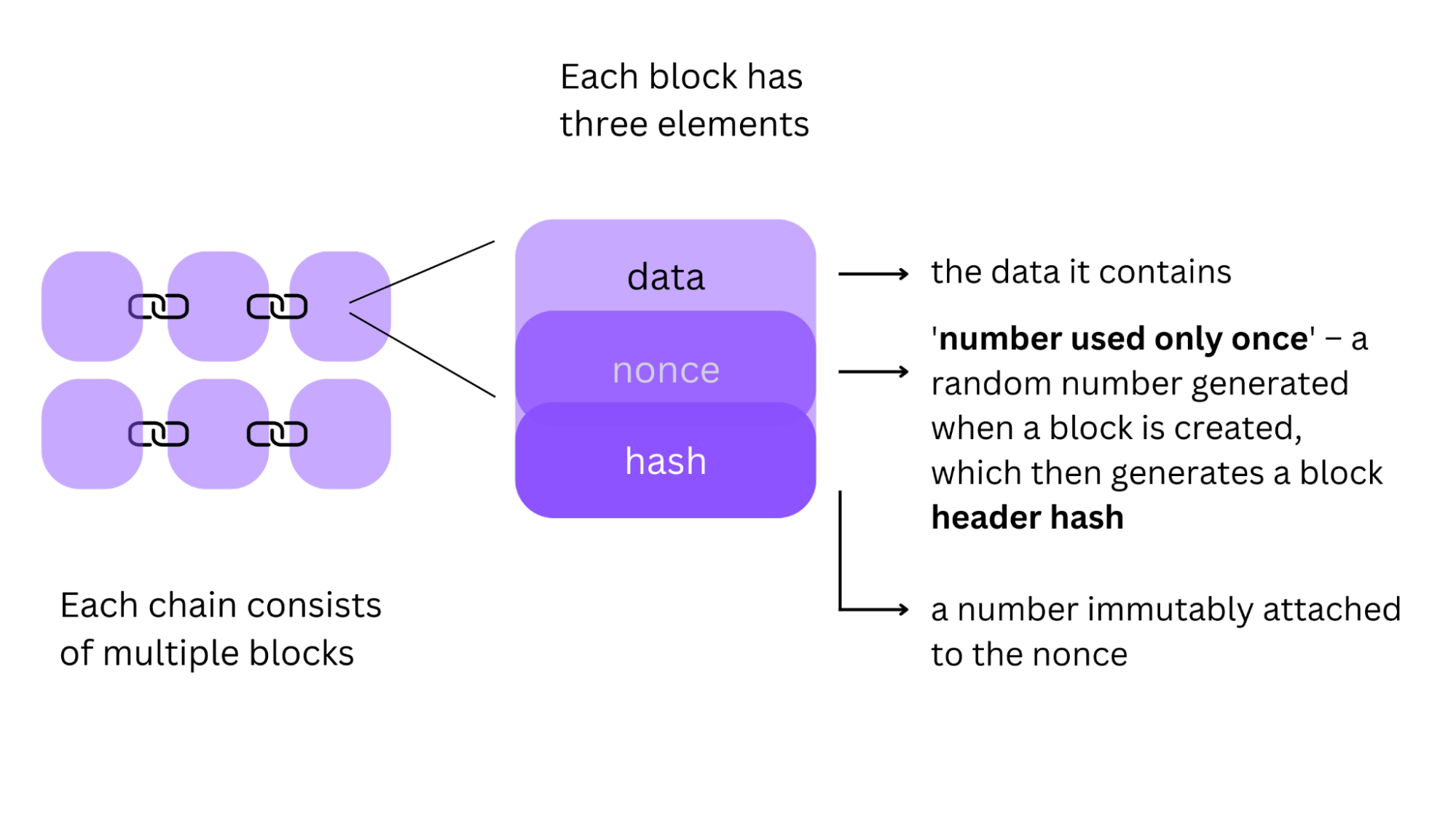

So, why is it called a blockchain? This one's easy: because the digital ledger is made up of virtual blocks of data which are, you guessed it, chained together. We'll go into exactly how this works in a bit.

Blockchains can record and validate all sorts of transactional data. While they are currently most used for cryptocurrency transactions, they can be used for healthcare records, supply chain transactions, property information – pretty much anything.

What is a blockchain’s purpose?

The purpose of a blockchain is to create an immutable record of information that's independently verified by, and distributed across, multiple sources.

…but why?

Well, to understand that, you need to understand why blockchain technology is special. The fundamental difference between a blockchain and a typical database is the way that the data is stored.

Where a typical database may use a table, for example, data is stored on the blockchain in blocks, which are organized chronologically. When one block is full, it's chained onto the last one, and the next one starts getting filled, and so on and so forth. This means that the data is locked in a linear timeline that cannot be altered or undone, which makes it an exceptionally hard system to hack.

This is why the main purpose of a blockchain tends to be to record transactions, because its decentralized nature and method of storing data makes it very secure.

The history of blockchain

The most common application of blockchain technology at the moment is digital currency (crypto), which is where the concept was originally brought to life.

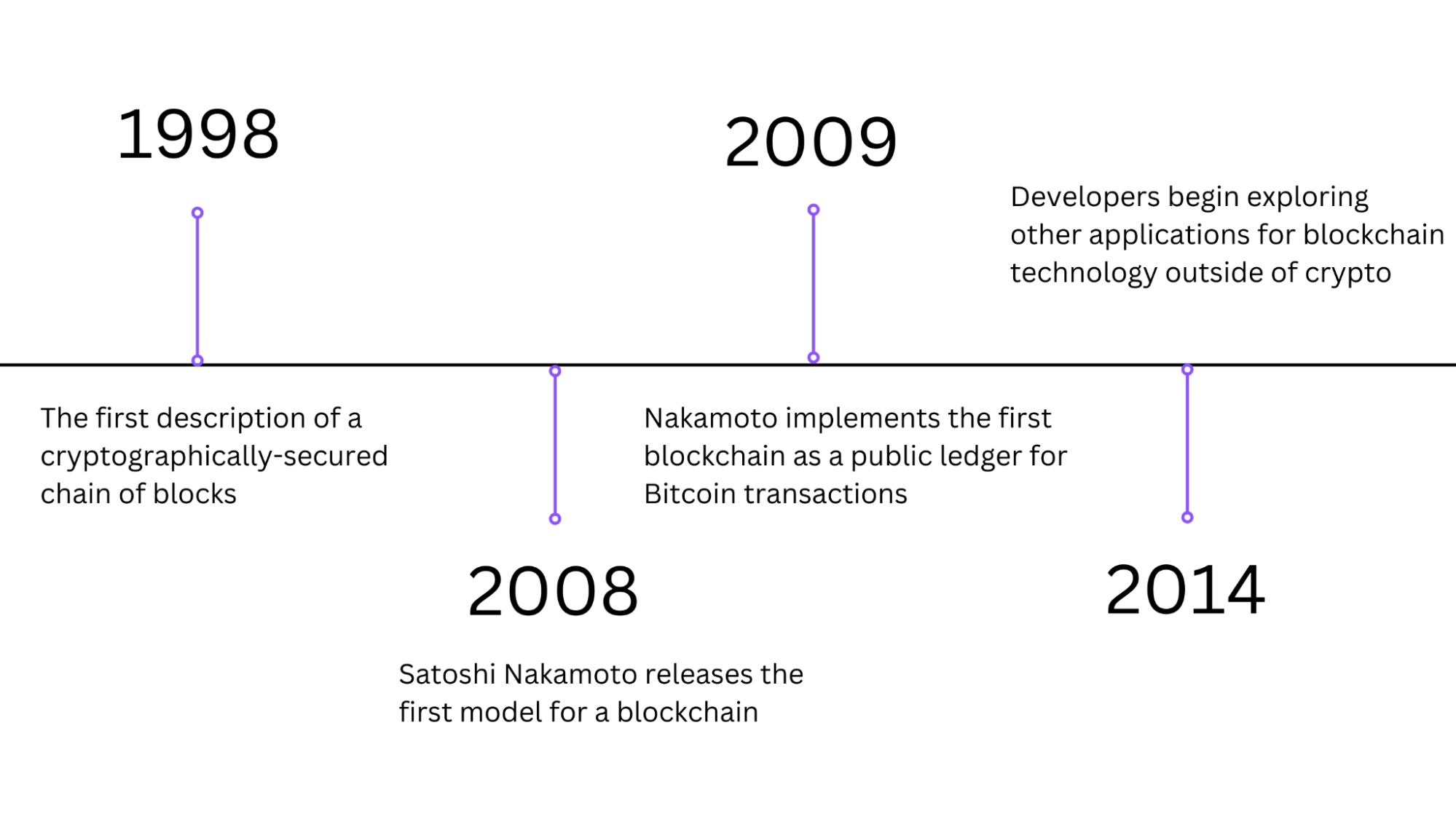

The first description of a cryptographically-secured chain of blocks was published by Stuart Haber and W. Scott Stornetta in 1991. It wasn't until 2008, though, that the original model for a blockchain was released in a whitepaper by the Bitcoin developer(s), working under the pseudonym Satoshi Nakamoto. A year later, the Bitcoin blockchain, the first of its kind, was implemented by Nakamoto as the distributed ledger technology for Bitcoin transactions.

For five years, the only application of blockchain technology was as the digital ledger for Bitcoin transactions. In 2014, though, the blockchain technology was finally separated from digital currency, and developers began exploring its potential for other applications. Later, the Ethereum blockchain emerged, including computer programs in the blocks in the form of game-changing smart contracts. That's a story for another day, though.

How does a blockchain work?

We're not going to go into too much technical detail here, as it can get quite complicated, so we're just going to cover the basics.

Here are the three main things you need to know to understand how blockchains work.

Types of blockchain networks

The first thing to know is that there are actually four types of blockchain networks:

Public blockchain networks

This type of blockchain network is permissionless (users don't need any kind of permission to use it), open (anyone can join), and fully decentralized. This means that all nodes have equal rights to create and validate blocks. Public blockchains are most commonly used for exchanging and mining cryptocurrencies.

Private blockchain networks

A private blockchain network is controlled by a single organization and requires nodes to have permission. Unlike a public blockchain, a central authority will decide who can be a node and the rights each node has. Private blockchains are only partly decentralized as public access to them is restricted.

Consortium blockchain networks

This type of distributed network requires permissions, but is governed by a group of businesses. As such, they have higher levels of decentralization, but not as much as public blockchains.

Hybrid blockchain networks

Hybrid networks are essentially a combination of public and private blockchains in that they are centrally governed, but require a public blockchain to perform certain transaction validations.

Consensus mechanisms

The second thing to know is that blockchains require something called a consensus mechanism to function. In simple terms, a consensus mechanism is a blockchain protocol that helps verify and validate transactions. There are two types of consensus mechanisms:

Proof of Work (PoW)

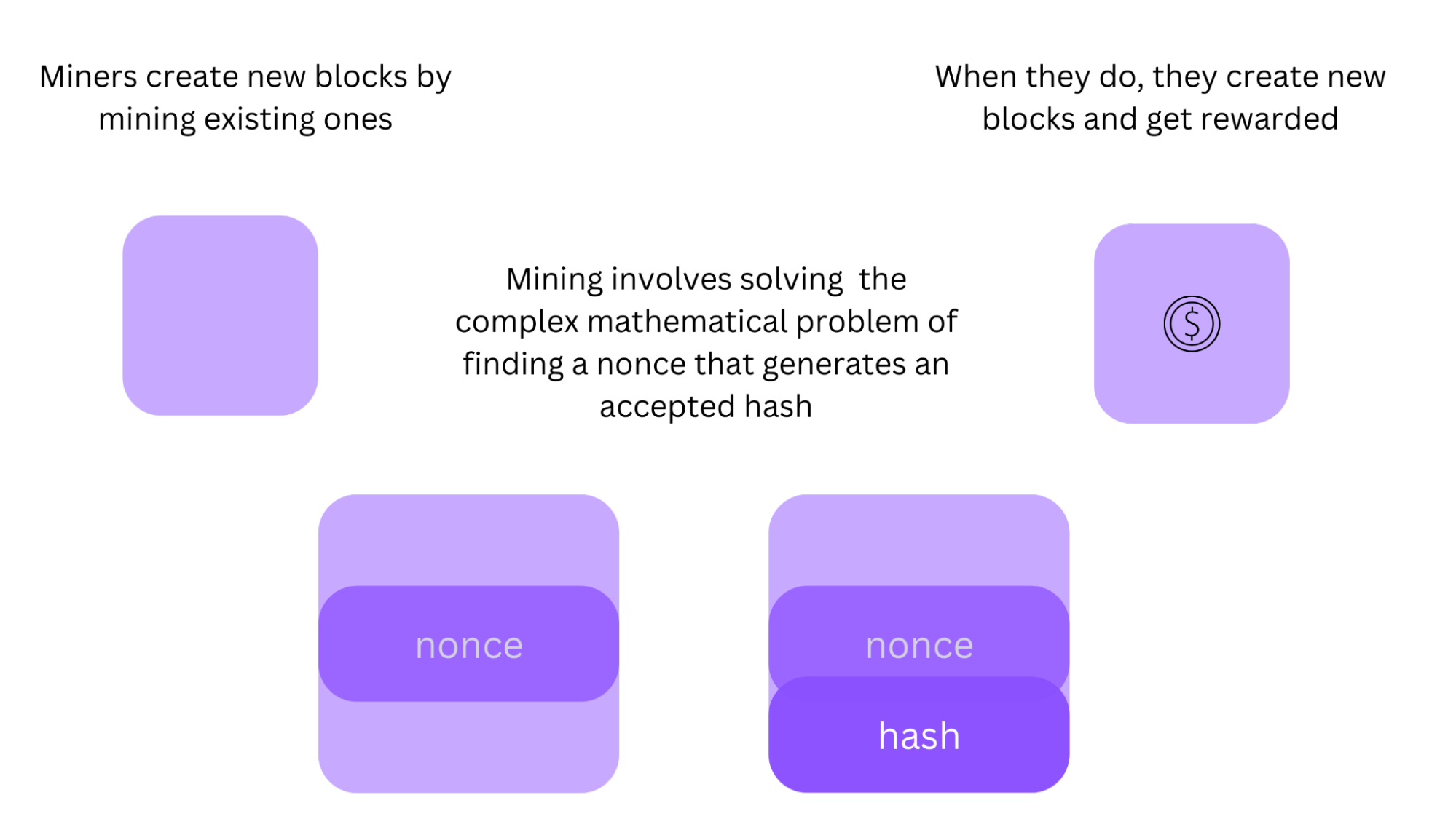

Proof of Work consensus mechanisms use a process called mining, in which transactions are validated by lots of different computers racing to solve a complex mathematical problem. The main benefit of this is how difficult it is to manipulate the data. A major drawback, however, is that it requires a huge amount of energy.

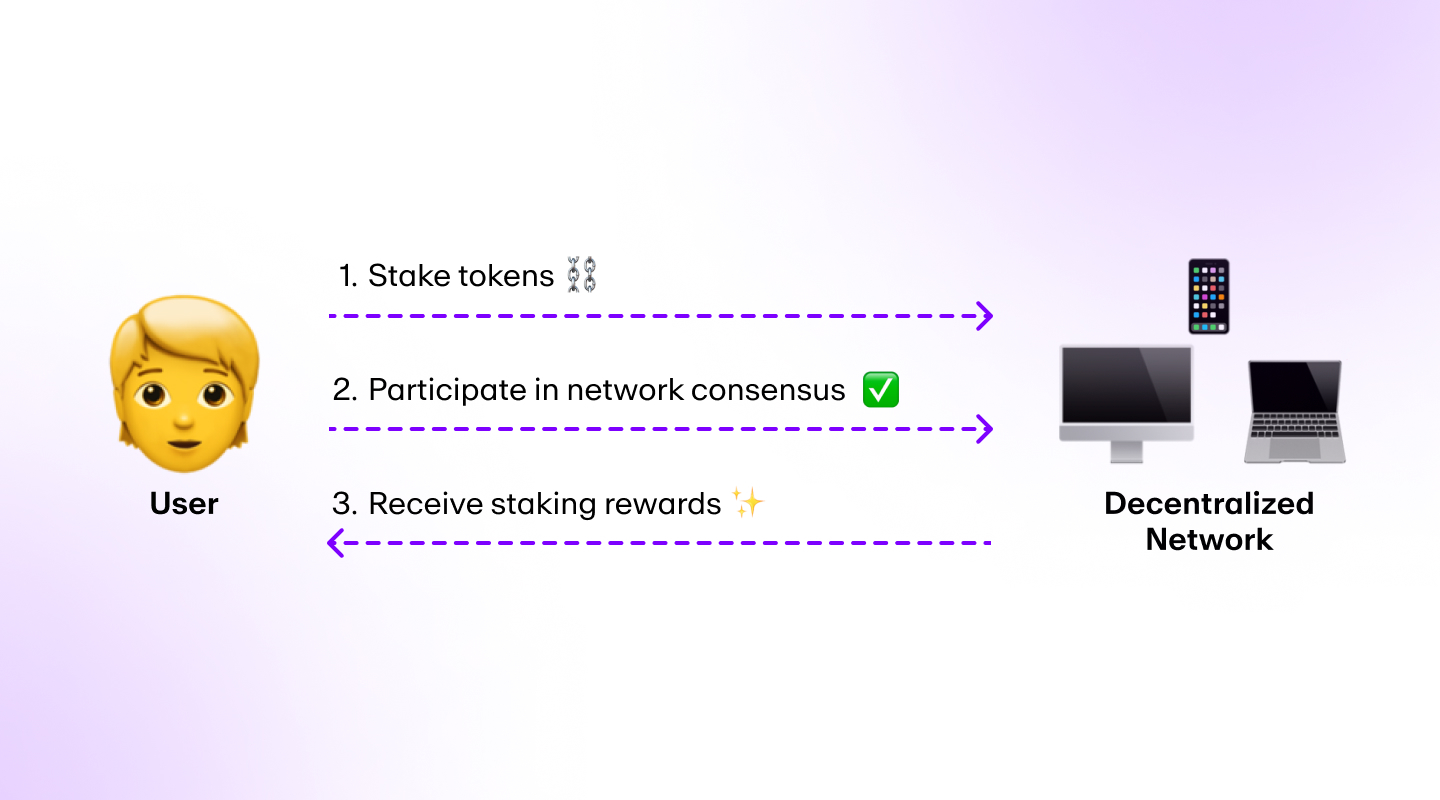

Proof of Stake (PoS)

Proof of Stake came about as an answer to this energy problem. This method requires less computing power because validators (the ones solving the math problems) “bid” to do so, rather than the first-come-first-serve approach of PoW.

Lingo

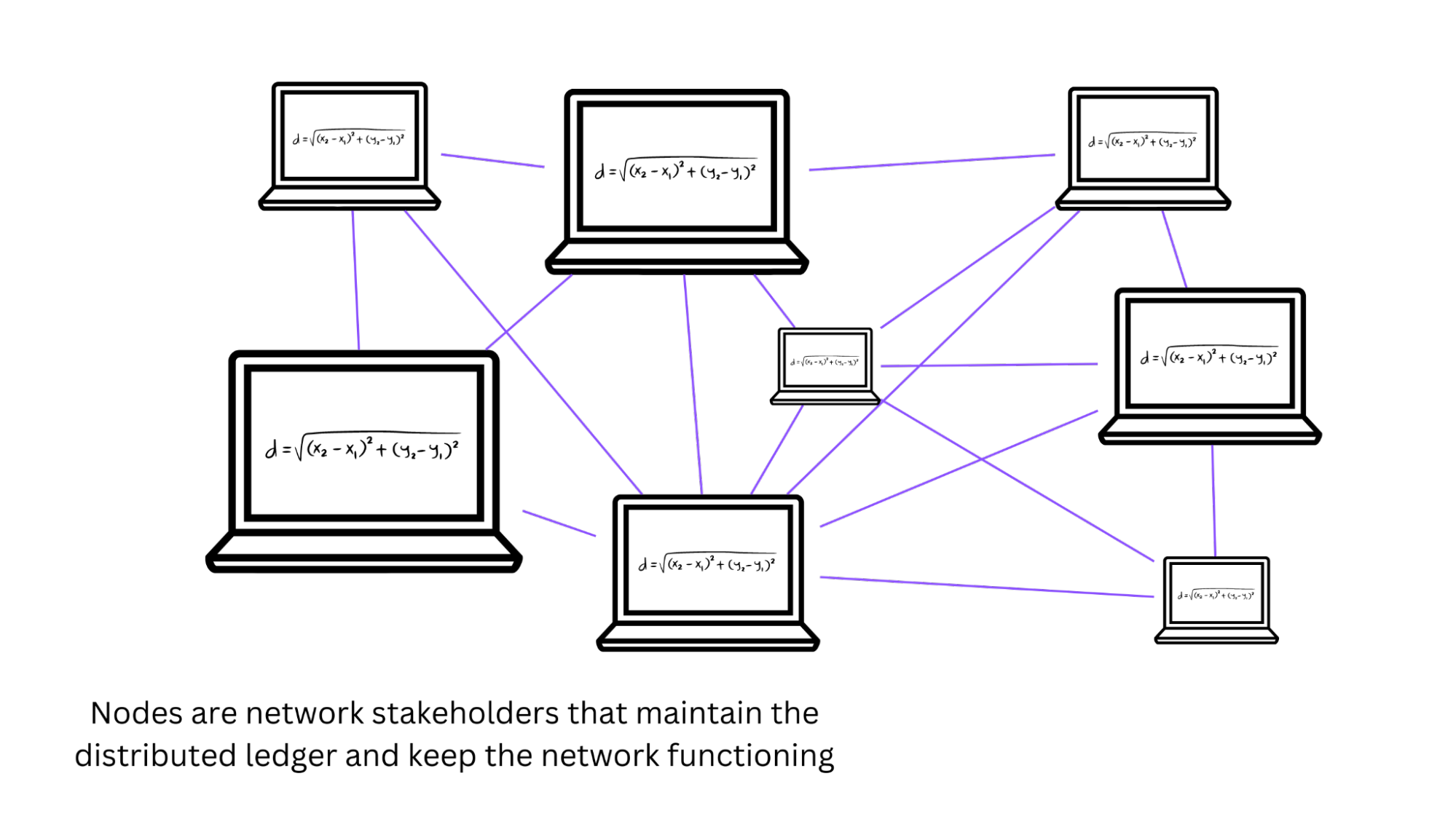

The third thing you need to know is a bit of the blockchain lingo. In traditional PoW blockchains, there are three key concepts: blocks, miners, and nodes.

Blocks

Miners

Nodes

The blockchain transaction process

Now that we have a bit more of an understanding of the building blocks (pun intended) of a blockchain, we can go into how it facilitates transactions. For ease of explaining, let's take financial transactions.

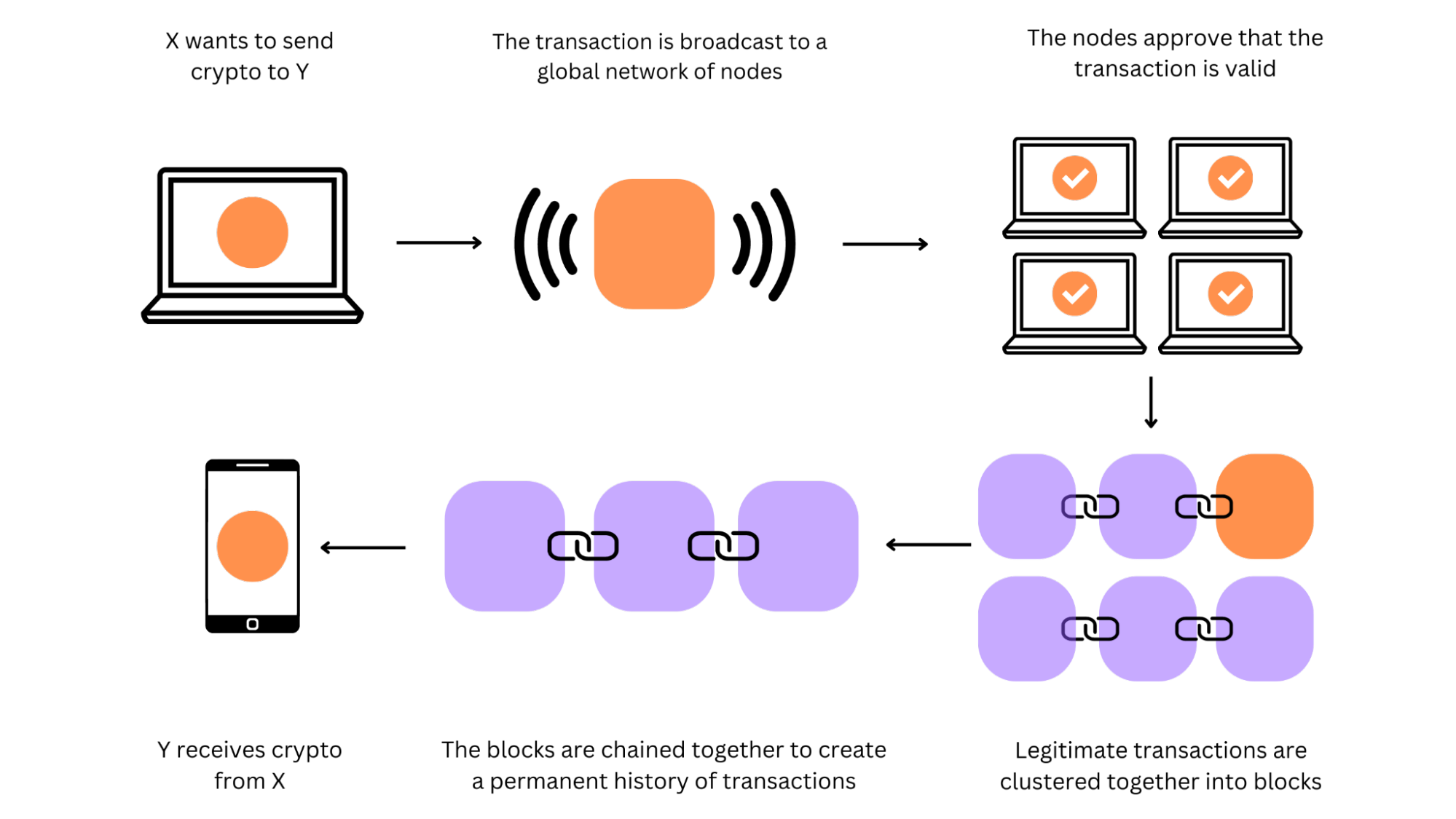

Let's say Person X wants to send some crypto (like Bitcoin) to Person Y. Person X will go into their wallet and fill in the details of the transfer. This transaction request is broadcast to the global network of nodes. The network will then solve those complex mathematical problems we discussed earlier to validate the transaction.

Once the transaction is confirmed, it joins others to form a block. These blocks are chained together to create a permanent history of transaction records, and then Person Y receives the crypto from Person X.

All Persons X and Y see, though, is the crypto leaving one wallet and entering another. Pretty cool.

Blockchain transparency

The transparency of blockchain refers to the fact that each and every transaction is recorded and visible (in public blockchains, they're visible to anyone – this will be slightly different in private blockchains, as well as consortium, and hybrid chains). To access a public blockchain, you either need to have a personal node, or use a blockchain explorer like Etherscan or XRPScan.

Using either one of these tools, you can view and track transactions across the chain. And, as every participant (or person making a transaction on the chain) has a unique alphanumeric identification number, you can see who's making the transactions.

Paradoxically, though, what you can't see is the identity behind the identification number. So within an entirely transparent system, there is also complete anonymity.

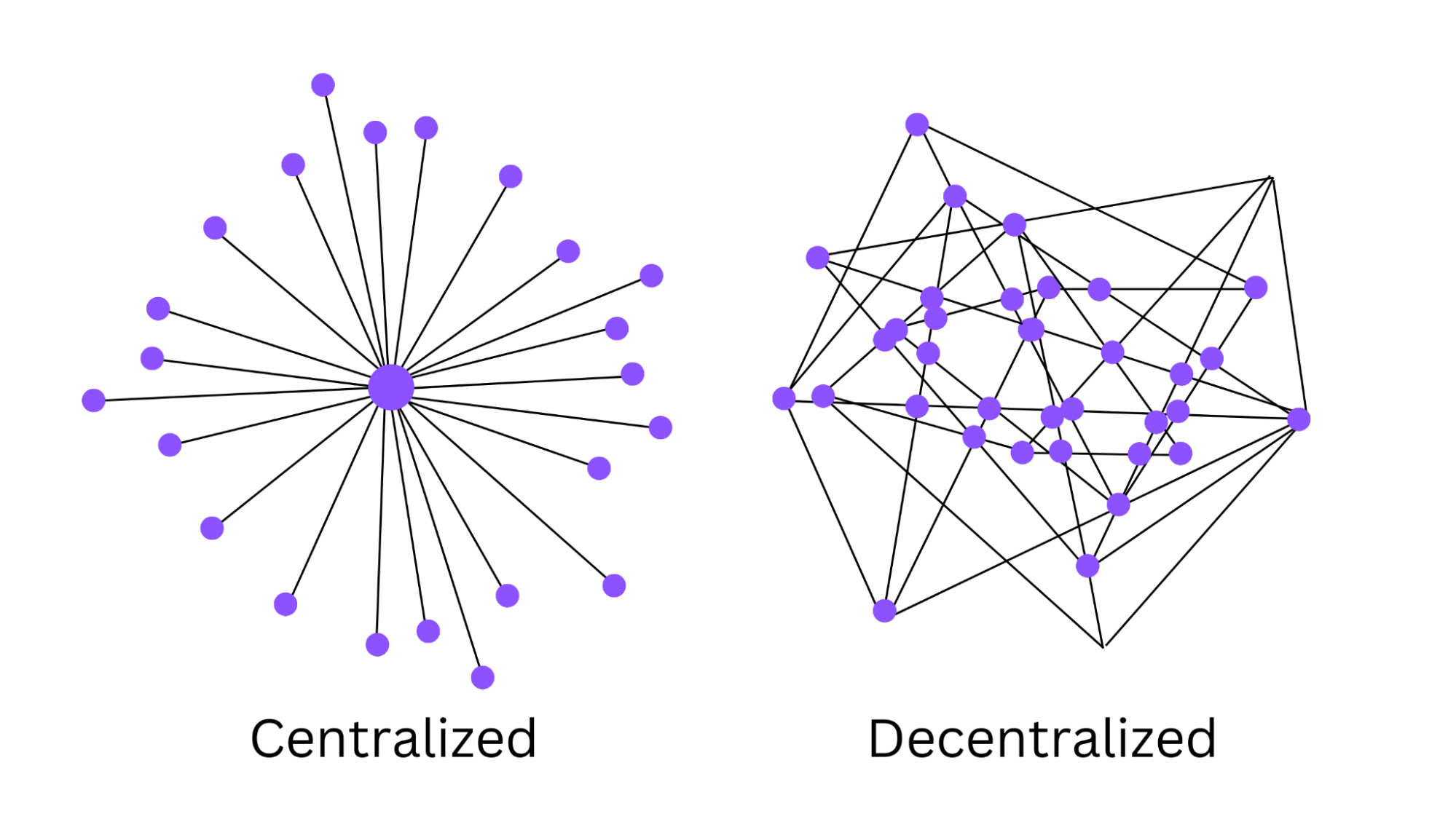

Blockchain decentralization

This decentralization word has popped up a lot so far, and you'll rarely see anything that mentions blockchain without mentioning it too. So how does it work, and why is it important?

Well, the key is those nodes we've been talking about. As we know, blockchains are made up of multiple nodes, and each of those nodes has a shared copy of the blockchain that is constantly being updated and validated by all of them in real time. This means three things:

- No single entity “owns” the chain (in a public blockchain network). Instead, it is equally shared across all the nodes so there can be no single point of failure.

- Changes have to be validated by multiple nodes. If an attempt is made to alter information on a single node, the others will cross-reference to see if it has been validated elsewhere. If it hasn't, it won't be added to the chain, and the node with the incorrect information will be identified.

- The information contained in the chain is entirely immutable, because once the nodes have validated it, it is locked in the chain forever.

Did you know? Any kind of electrical device that can maintain copies of the chain and keep the network functioning can act as a node.

This kind of decentralization is revolutionary, because it means there is no reliance on any central authority to provide security. Instead, the security is inherent in the fundamental transparency of the decentralized ledger and the complex mathematical system behind it.

Is blockchain technology secure?

The short answer is yes, blockchain is secure. And you already know why: decentralization, transparency, and the infrastructure of the system itself.

The slightly longer answer is how, and it's all to do with those hard working nodes. As we know, nodes work away to validate and verify transactions (and information), so they're constantly cross-checking with each other. When they agree a transaction is legitimate, it's added to a block, and when that block is full, it's added to the chain.

The chain is, therefore, a chronological, linear timeline of transactions. Just like time, you can't go back and alter a block that's already been added to the chain. The only way to do that is if a majority of nodes reached a consensus to do so (then they have the powers of a time machine). However, this is exceptionally rare, because nodes don't make mistakes. They can't, because there's so many of them constantly verifying each other.

So, the only way to alter information – for example, if a hacker wanted to go in and steal using their own node – is a majority consensus. This is where we get the phrase “51% hack”, because 51% of the nodes would have to validate a single bad actor's alteration. The sheer amount of money, time and resources needed to do this means it's virtually impossible. And even if it were to be achieved, all the other nodes would notice the drastic changes, and those members would fork off to form a new blockchain branch.

This level of security is just one of many benefits of blockchain technology though. Let's take a look at some of the others.

Pros and cons of blockchain technology

There are benefits and drawbacks of any distributed ledger technology like blockchain.

Blockchain advantages

Accuracy

The use of consensus mechanisms when it comes to recording transactions in a blockchain network means accuracy is greatly improved compared to paper or process-heavy systems.

All nodes are working in sync across the entire network to verify and validate transactions in real time, so records within a blockchain's distributed database have a much smaller likelihood of error than other methods of record keeping.

Transparency

We've touched on this already throughout this article, but one of the biggest benefits of blockchain technology is its transparency. Partly because the fundamental transparency of the entire blockchain system is what paves the way for all the other benefits, but also because it enables a sense of trust to exist that is almost impossible to come by otherwise.

A blockchain network enables trust between two parties that have no prior relationship, because they can rely on the accuracy and transparency of the blockchain network.

Reduced costs

With blockchain technology being increasingly used for applications beyond financial transactions, it's becoming clear just how much of a cost-saving tool it can be.

By drastically reducing the number of manual tasks, boosting the efficiency of auditing processes, and automating things like payment processing or recording transactions, blockchain technology can streamline operations and remove the cost of “middleman” roles for businesses.

Decentralization

We've mentioned this one a lot, but it's because it's one of the key benefits of blockchain systems. Since the blockchain network is almost impossible to cheat, there is no need for a central entity that verifies or validates data.

This allows the middleman to be taken out of all kinds of processes from monetary transactions to supply chains. Trust is built into the blockchain infrastructure, which means there's no need for a governing body that adds steps, costs, and inefficiency to a process. Speaking of efficiency...

Efficient transactions

A huge advantage of blockchain platforms – particularly within the financial space – is that they enable transactions to be faster and more efficient. With typical financial institutions, you may have to wait days for a transaction to be approved, and on top of that, you may have to pay transaction fees.

With a blockchain platform, however, you're not hindered by opening hours or availability. Transactions can happen immediately because they don't rely on a central approver (that you have to pay to use). And with quicker processing times, blockchain technology also allows for minimal transaction costs.

Banking the unbanked

Last, but certainly not least, is the access that cryptocurrency (which runs on blockchain) opens up to people all over the world.

Traditional currencies require a bank account, which in turn requires personal information like an address and/or an ID of some kind. Billions of people (1.7 billion adults, to be exact) don't have a bank account where they can store their wealth, so they rely on cash.

Cash, however, is hard to manage, easy to steal, and exceptionally difficult to transfer to the other side of the world. Cryptocurrency wallets don't require anything other than an email address to open, are a much safer way to store wealth, and have revolutionized international remittances.

Blockchain disadvantages

Energy cost

While blockchain technology can save businesses and individuals money thanks to its efficiency and lack of transaction fees, it is by no means a free service. PoW blockchain systems in particular eat up energy because of all the nodes competing to solve the problems quickest to earn the block rewards.

While PoS systems address this energy usage, that still leaves the cost of the miners; if they aren't incentivized by mining cryptocurrency (which may not be the case for blockchain's other applications), their cost will need to be met in other ways.

Inefficiency

Blockchain networks are incredibly efficient in some ways, but also inefficient in others. For example, the Bitcoin network takes up to ten minutes to add a new block to the chain, which translates to about seven transactions processed per second. Compare this to Visa, for example, which processes 65,000 transactions per second.

There's the issue of how much data each block can hold. At the moment, block sizes are still relatively small, which raises issues around the scalability of the technology.

Illegal activity

Something people are often concerned about when it comes to cryptocurrencies and blockchain networks is their use for criminal or illegal activity. Blockchain can and has been used for scams and fraudulent transactions because it's possible for people to hack the funds of unsuspecting victims or use a blockchain platform to anonymously make illegal purchases.

However, the number of illicit transactions has vastly reduced on bigger networks like the Bitcoin blockchain as it's matured. It's worth noting that many argue that the good applications of blockchain (such as banking the unbanked) outweigh negative uses.

Regulatory uncertainty

As the most popular blockchain networks continue to grow, governments are more inclined to regulate them. While this is exceptionally difficult given blockchain's decentralized nature, it is possible for governments to outlaw the participation in cryptocurrencies altogether.

How can blockchains be used in the real world?

While blockchain was born to run the Bitcoin network, its uses now extend far beyond currency and private transactions. In fact, most industries could benefit from the use of blockchain technology.

Here are a few examples of industries that have already started to adopt blockchain technology:

Healthcare

Blockchain platforms are an incredibly useful and efficient way to store and exchange patient data, but they can also be used to identify mistakes in the medical field (all those nodes have to come to a consensus, remember).

Property

Blockchain could be used in real estate, not simply to keep property records, but also to tokenize tangible assets and increase efficiency across underlying industry operations.

Supply chain

Huge food supply chains, like IBM Food Trust, are already using blockchain technology to trace the end-to-end journey of food products, allowing for quick identification of contamination points and transparency over everything the product has come into contact with.

Voting

Voting systems across the world are in need of some technological innovation, and blockchain could provide a solution. A voting system that makes use of blockchain technology offers the potential to drastically reduce (if not entirely eliminate) voter fraud. This means more time and money saved on human resources and increased transparency across the voting process.

Blockchain FAQs

What's the difference between blockchain and Bitcoin?

Since the first blockchain was used for Bitcoin, it's no surprise that many people confuse the two.

It's important to note, however, that Bitcoin and blockchain are not the same thing. Bitcoin is a cryptocurrency, and blockchain is the decentralized, distributed ledger technology that it runs on.

While the Bitcoin blockchain is still the largest to date, it is far from the only one. Other popular blockchains are Ethereum (ETH), Binance Smart Chain (BNB), Solana (SOL), XRP (XRP), and Cardano (ADA).

What is block time?

Block time refers to the time it takes for new blocks to be added to the blockchain. While all blockchains share a linear structure (blocks are added one after the other chronologically), not all of them add blocks at the same frequency, as it depends on the particular protocol on which the blockchain was developed.

As an example, though, the Ethereum blockchain adds new blocks every 12 seconds (Ethereum.org), the Solana blockchain adds new blocks every 21 - 46 seconds, and the Algorand blockchain adds new blocks every five seconds.

Begin your blockchain journey with MoonPay

Now that you know the basics of blockchain technology and distributed ledgers, it's time to experience blockchain for yourself.

To get started, simply buy Bitcoin or your preferred cryptocurrency via MoonPay using your credit card or any other payment method.

.png)